Introduction

Cell and gene therapy (CGT) represents a groundbreaking frontier in modern medicine, offering innovative treatments for a wide range of diseases. CGT therapies provide personalized and potentially curative life-long solutions where traditional treatments fall short. In recent years, the CGT landscape has evolved rapidly, with advancements in gene editing technologies like CRISPR, the rise of CAR-T cell therapies, and a growing number of regulatory approvals. However, despite its promise, the field faces challenges such as manufacturing complexities, high costs and reimbursement issues, and regulatory hurdles. This deep-dive report provides an update of the previous Cell and Gene Therapy Clinical Trials – 2024 Edition, exploring the 2022-2024 state of CGT clinical trials landscape.

Research Methodology

We analyzed the activity of over 250 companies (Ιmage 1) that between 2022 and 2024 have been involved in clinical trials in the Cell and Gene Therapy space either as a sponsor or as a collaborator to:

1) Identify the top Therapy Areas (TAs) toward which Cell and Gene Therapy research is directed (we used the terms provided for conditions/indications by clinicaltrials.gov, in order to categorize the trials into broader therapeutic areas /categories)

2) Identify and rank the top players (sponsors or collaborators) by the number and Phases of CGT clinical trials they are associated with

3) Find out how the number and phase of clinical trials have evolved from 2022 to 2024

Clinical trials included in the analysis

For the purposes of the analysis, the trials that were delivered as results from clinicaltrials.gov when searching for the keywords “Cell Therapy OR Gene Therapy” and met the criteria below were considered.

List of criteria:

• Starting date between 2022 and 2024

• For industry-sponsored trials, we selected the studies based on their funding type. For trials that listed an industry collaborator, we automatically identified relevant companies from the dataset. Only those companies with Protocol Registration and Results System (PRS) accounts at ClinicalTrials.gov were included in the “industry collaborator” analysis.

• We included trials with the following status: Active, Not recruiting, Available, Completed, Enrolling by Invitation, Not yet Recruiting, and Recruiting

• We also included trials with the following Phase status: Early Phase 1, Phase 1, Phase 1|Phase 2, Phase 2, Phase 2|Phase 3, Phase 3, Phase 4 (trials whose Phase was either not specified or not applicable were not considered)

Key findings

Shift from Oncology to Non-Oncology Indications in Cell and Gene Therapy Trials

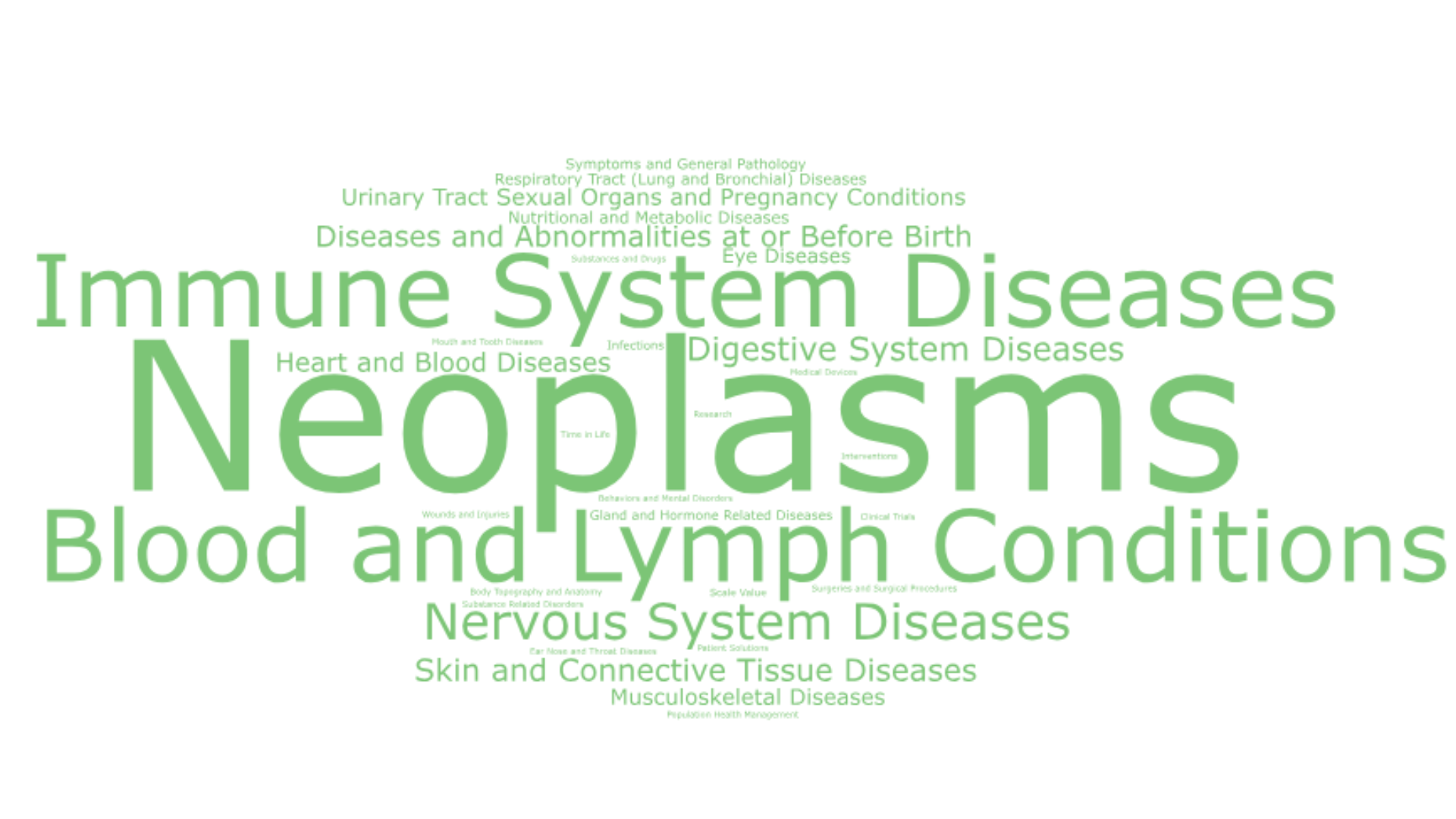

The Top 3 therapeutic areas where CGT research is applied are neoplasms, blood and lymph conditions, and immune system diseases (based on the absolute count of appearances of each TA in the complete dataset of clinical trials analyzed).

Figure 1 shows the number of times each one of the Top 16 TAs appeared in the dataset per year (2022-2024), and the word cloud in Image 1 shows all the different TAs included in the dataset. While the focus on oncology research is clear, we observe that especially for 2024, there’s a shift toward non-oncology indications and a growing CGT pipeline for blood and lymph conditions, immune and nervous system diseases as well as urinary tract, sexual organs and pregnancy conditions, musculoskeletal and skin and connective tissue diseases.

Specifically, between 2022 and 2023, the shift from oncology to non-oncology indications was 17.25%, whereas between 2023 and 2024, this percentage rose to 33.81%. That finding is in accordance with the Gene, Cell, & RNA Therapy Landscape Report from ASGCT and Citeline, according to which “across 2023 there has been a consistent trend of an increasing proportion of initiated trials each quarter that target non-oncology indications, rising from 39% of trials started in Q4 2023 to 51% of trials started in Q2 2024’’.

The Dual Role of Industry in Clinical Trials: Sponsor and Collaborator

We categorized clinical trials based on whether the industry acted as the sponsor or a collaborator, and performed separate analyses for each group. Figure 2 presents the absolute number of trials (selected according to the criteria described in the Research and Methodology section) involving industry as either sponsor or collaborator from 2022 to 2024. In cases where industry served as a collaborator, the sponsor were hospitals, universities, networks, the NIH, and government agencies.

In Figure 2, we see a growing role of industry in CGT trials both as a sponsor and a collaborator over the years, reflecting the field’s increasing interest and evolution. Notably, the number of trials with industry as a collaborator doubled between 2022 and 2024, emphasising that such partnerships, given the complexity and costs of CGT research, are not just common, but crucial for achieving success.

Collaborations in the field are important because they accelerate innovation and overcome manufacturing challenges. Combining resources, expertise, and infrastructure speeds up clinical development. For example, academic medical centers (AMC) possess a broad range of expertise across disciplines such as cell biology, bioengineering, and clinical delivery. By utilizing existing equipment and facilities, including cleanrooms and bioreactors, AMC can support the complex development processes required for CGTs. Also, AMCs can co-locate therapy manufacturing and patient treatment facilities. This proximity simplifies the supply chain, enhances the quality of cell products by reducing the need for transportation-related freeze-thaw cycles, and streamlines the administration of autologous therapies.

Additionally, collaborations could ease regulatory pathways, since pharma partners could help navigate FDA/EMA regulations for new therapies. Finally, collaborations contribute to enhancing market access as hospitals involved in CGT trials and research institutions could provide direct access to patients, while pharmaceutical companies use their distribution infrastructure, marketing expertise, and expanded access initiatives to promote and deliver both the therapy and the supporting research.

Increased Chinese Involvement in CGT Clinical Trials and Expanding R&D Efforts in Rare Diseases

Figures 3 and 4 present the top companies participating in CGT clinical trials by developmental stage from 2022 to 2024, with industry acting as sponsor (Figure 3) or collaborator (Figure 4). Notably, many of these companies, such as Shanghai Cell Therapy Group, Frontera Therapeutics, GeneCradle, Nanjing Legend, and Yake, are based in China. This observation aligns with our previous findings, which showed a significant rise in the number of Chinese clinical trial sites between 2019–2023 compared to 2014–2018. Several factors may explain China’s leading role, including a supportive regulatory environment, ample funding opportunities, and a large population with unmet medical needs.

Oncology Continues to Dominate Rare Disease CGT Development, but Non-Oncology Efforts Are Growing

According to source (1), the majority of rare-disease-focused gene therapy development (53%) is still in oncology, while the remaining 47% targets non-oncology conditions. An examination of the company pipelines shown in Figures 3 and 4 confirms that oncology remains a key area of focus, yet CGT research is increasingly branching into rare non-oncological diseases.

For example, Johnson & Johnson, Shanghai Cell Therapy Group, Genentech, AbbVie, and Iovance concentrate on oncology therapies. Meanwhile, Frontera Therapeutics is developing treatments for eye diseases (e.g., X-linked retinitis pigmentosa, diabetic macular edema, and neovascular age-related macular degeneration), and Sarepta Therapeutics focuses on limb-girdle and Duchenne muscular dystrophy. GeneCradle’s pipeline includes spinal muscular atrophy and Pompe disease, while Kyverna targets Stiff-Person Syndrome, sclerosis, myasthenia gravis, and lupus nephritis. Pfizer’s CGT portfolio spans both hematologic malignancies and rare diseases such as hemophilia (although according to recent news hemophilia gene therapy has been deprioritized by the company) and Duchenne muscular dystrophy.

This growing emphasis on rare diseases suggests a shift from broad-market treatments to more highly personalized therapies. Advances in AI and genomic research are accelerating the diagnostic process and helping make many previously “orphaned” conditions financially and clinically viable for drug development.

Figure 3: Top 11 companies that sponsored the most CGT clinical trials in all Phases of development from 2022 to 2024. Data presented as absolute numbers of clinical trials.

The number of CGT trials across developmental Phases increased from 2022-2024

Figures 5 and 6 illustrate the evolution of CGT trials from 2022 to 2024, highlighting industry participation as either a sponsor or collaborator. Overall, the number of CGT trials across all Phases increased year over year, with particularly notable growth in early-stage trials. However, 2022 saw a marked dip in the number of early-Phase (Phase 1 and Phase 2) trials, likely due to the lingering effects of the COVID-19 pandemic, as detailed in our previous report.

Following the pandemic, from 2022 to 2023, there was a strong rebound in early-stage CGT trials, which continued to accelerate into 2024. Notably, a substantial increase in early-stage clinical trials (Phase 1 to Phase 2/3) involved industry acting as a collaborator.

Legislation and regulatory frameworks updates, the multiple regulatory approvals (as of June 2024, a total of 100 approved products globally according to Cell and Gene Therapy Global Regulatory Report from ISCT and Citeline), as well as increased biotechnological knowledge and innovation, are among the main reasons for CGT field evolution. During 2024, agencies like EMA FDA issued guidelines to ensure the safety, efficacy, and quality of these advanced therapies. For example, EMA issued guidance on the structure and data requirements for a clinical trial application for investigational ATMPs, and a reflection paper discussing the use of RWD in non-interventional studies to generate real-world evidence. FDA issued guidance on potency assurance for the CGT products, and a guidance for the industry related to considerations for the use of human- and animal-derived materials in the manufacture of cell and gene therapy and tissue-engineered medical products. All FDA guidance for CGT can be found here.

Figure 6: Yearly distribution of cell and gene therapy trials (with industry as collaborator) across Phases

Conclusion

By analyzing the CGT clinical trials landscape from 2022-2024, we identified that neoplasms, blood and lymph conditions and immune system diseases are still the main therapeutic areas where CGT is applied. While oncology indications are the main area of CGT research, the field seems to be accelerating its diversification efforts beyond oncology indications, to support therapies for rare diseases.

A dynamic interplay of regulatory approvals, the broader regulatory landscape, and the ongoing evolution of knowledge, research, and innovation, collectively foster the development and advancement of CGT space which is shown by the continuously increasing number of clinical trials year-over-year. Additionally, we observed that China continues to be an attractive, growing market for CGT.

Finally, clinical trials with industry as a collaborator doubled from 2022 to 2024, showcasing that collaborations in the CGT field are crucial since they help bridge the gap between scientific innovation and real-world application through acceleration of clinical development, cost reduction and improved patient access; ultimately bringing groundbreaking therapies to market faster and more efficiently. The industry’s preference for collaboration in CGT clinical trials appears to be a multifaceted strategy driven by both the desire to de-risk investments in a complex and costly field and the need to acquire expertise for diversifying into non-oncology indications.

For any questions / comments or other feedback or to find out more about how your company can accelerate success in the cell and gene therapy space with LucidQuest, contact us at info@lqventures.com

#CellAndGeneTherapy #Biotech #ClinicalTrials #RareDiseases #Innovation #RegenerativeMedicine #Pharma #CGT #LifeSciences #DrugDevelopment

Sources:

https://www.asgct.org/global/documents/asgct-citeline-q3-2024-report.aspx

https://www.iqvia.com/blogs/2024/02/partnerships-in-cell-and-gene-therapy-clinical-trials

https://www.fda.gov/vaccines-blood-biologics/biologics-guidances/cellular-gene-therapy-guidances

https://www.drugdiscoverytrends.com/100-cell-and-gene-therapy-leaders-to-watch-in-2025/